Sergio Ermotti, CEO of Swiss banking giant UBS, during the group’s annual shareholders meeting in Zurich on May 2, 2013.

Fabrice Coffrini | Afp | Getty Images

Switzerland’s tough new banking rules create ‘lose-lose situation’ for UBS and could limit its potential to take on Wall Street giants, according to Beat Wittmann, a partner at Zurich-based Porta Advisors.

In a 209-page plan published on Wednesday, the Swiss government proposed 22 measures aimed at tightening controls on banks deemed “too big to fail”, a year after authorities were forced to broker an emergency rescue of Credit Suisse. UBS side.

The government-backed takeover was the largest merger of two systemically important banks since the global financial crisis.

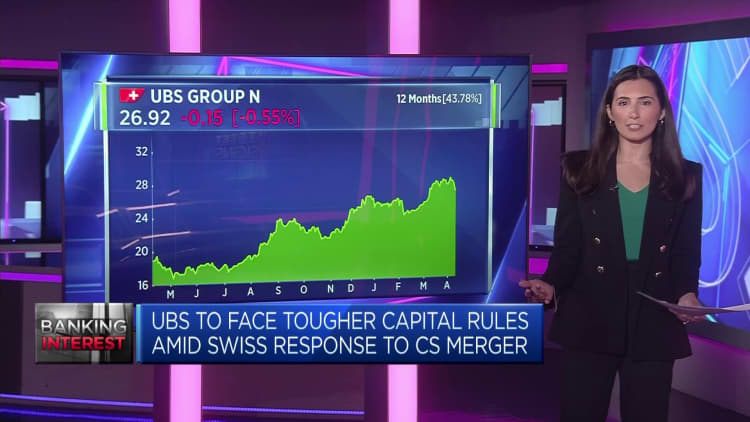

UBS’s $1.7 trillion balance sheet is now twice the country’s annual GDP, prompting closer attention to the safeguards surrounding the Swiss banking sector and the broader economy following the collapse of Credit Suisse.

Speaking on CNBC’s Squawk Box Europe on Thursday, Wittmann said Credit Suisse’s fall was “entirely self-inflicted and a predictable failure of government, central bank, regulatory and, above all, policy [of the] Minister of Finance.”

“Back then, of course, Credit Suisse had a failed, unsustainable business model and incompetent management, all of which was reflected in a steadily falling share price and credit spreads across the company. [20]22, [which was] is completely ignored because there is no institutionalized know-how at the policymaker level to monitor the capital markets, which is important in the case of the banking sector,” he added.

The report, published on Wednesday, called for more powers to be given to the Swiss financial market watchdog, the application of capital surcharges and strengthening the financial position of subsidiaries, but it did not recommend a “full increase” in capital requirements.

Wittman suggested the report does nothing to allay concerns about the ability of policymakers and regulators to oversee banks while ensuring their global competitiveness, saying it “creates a lose-lose situation for Switzerland as a financial center and for UBS, which cannot develop Own business”. potential”.

He argued that regulatory reform must be a priority, rather than tightening the screws on the country’s biggest banks, if UBS is to capitalize on its newfound scale and finally challenge banks like Goldman Sachs, J.P. Morgan, Citigroup And Morgan Stanley — which have similar sized balance sheets but trade at much higher valuations.

“It comes down to the playing field at the regulatory level. Of course, it’s about competencies and then about incentives and regulations, and regulations like capital requirements are a global challenge,” Wittmann said.

“It can’t be that Switzerland or any other jurisdiction would introduce completely different rules and levels there – it wouldn’t make any sense, then you wouldn’t be able to truly compete.”

For UBS to optimize its potential, Wittmann argued that the Swiss regulatory regime must be brought in line with those in Frankfurt, London and New York, but said Wednesday’s report showed a “lack of willingness to engage in any relevant reforms” that would protect the Swiss economy and taxpayers, but would allow UBS to “catch up with global players and US valuations.”

“The track record of Swiss policymakers is that we had three global systemically important banks and now we are down to one, and these cases were a direct result of insufficient regulation and enforcement,” he said.

“FINMA had all the legal basis, the tools to deal with the situation, but they didn’t apply them – that’s the whole point – and now we’re talking about fines, and to me it sounds like pennies and pound stupid.”