Today, enjoy the 0xResearch newsletter on Blockworks.co. Tomorrow, get the news delivered directly to your inbox. Subscribe to the 0xResearch newsletter.

Using blockchain metrics less wrongly

Blockchains churn out a lot of public data. In Crypto Twitter’s endless quest to pit Blockchain A against Blockchain B, investors, researchers and KOLs have no shortage of metrics to grapple with when making their case.

Bad use of numbers, however, often muddies the capacity to understand this world.

In today’s edition of 0xResearch, we’re looking at three metrics and their problems: active addresses, blockchain “profitability” and total value secured.

Active addresses

“Active addresses” tells us how many active, paying users are on a given protocol.

“Facebook has three billion monthly active users” is a useful statement that tells us something about the social network. Since there is no overwhelming profitable opportunity for spammers to flood Facebook, active addresses are a decent way to gauge how genuinely valuable the platform is to consumers.

But when it comes to blockchains, active addresses become less useful due to the ease of creating new wallets — and the overtly profitable opportunities to game airdrops or farm protocol incentives.

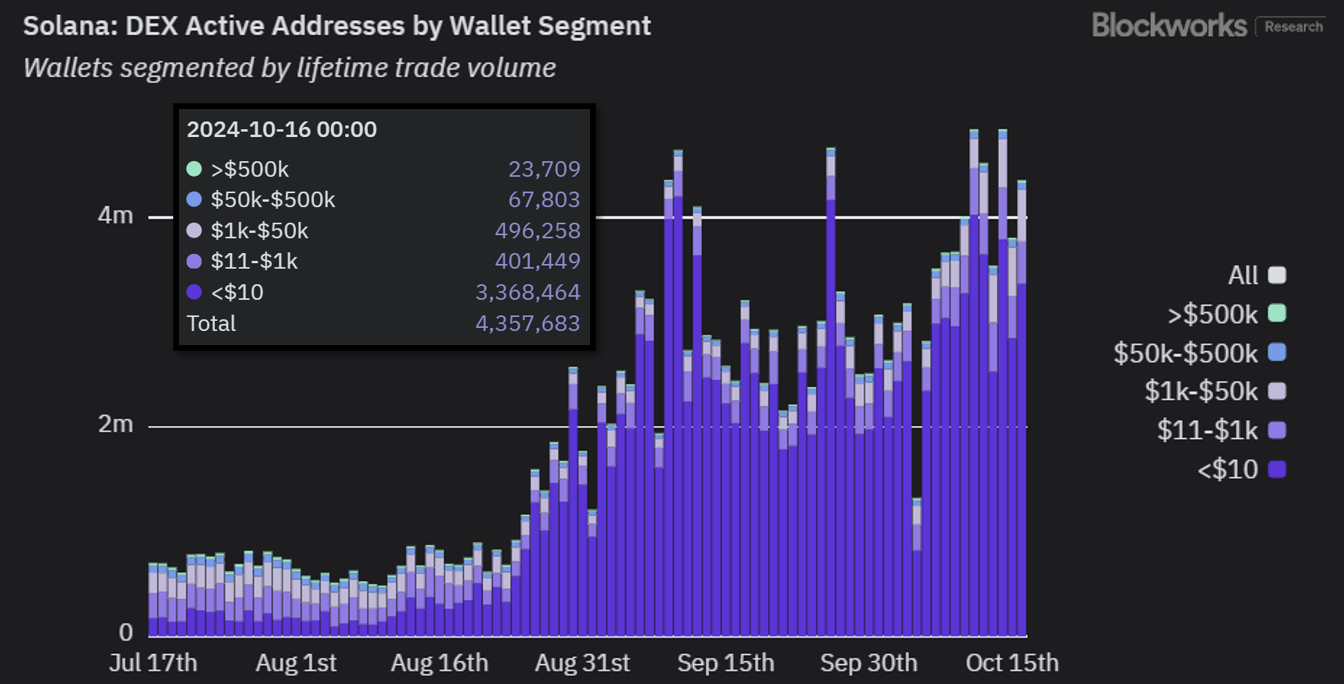

For instance, the following chart tells a clear story: Solana has had the largest number of daily active addresses in the last month, so Solana must be on a hot streak.

Most Solana users are trading on DEXs, so we should take a closer look at DEX activity. When we zoom into Solana’s active addresses on its DEXs, we see that the mass majority in the last day — about 3.4 million of a total 4.4 million — has traded less than $10 of lifetime volume.

This suggests spam or bot activity due to Solana’s cheap transaction fees rather than the number of “quality” users.

Here’s another example I wrote about previously: The Celo L1 (now an L2) saw its daily active addresses sending stablecoins shoot up to 646k in September. It surpassed Tron on the same metric, which prompted a shoutout from Vitalik Buterin and CoinDesk.

Upon closer scrutiny, Variant Fund data analyst Jack Hackworth found that 77% of these Celo addresses transferred negligible amounts of less than two cents, largely due to tens of thousands of users claiming a fraction of a cent from a universal basic income protocol known as GoodDollar.

In both cases, active addresses conveyed a story of high usage. But on closer examination, that story falls to the ground.

For more on this topic, look to Dan Smith, who has led the charge on the erroneous use of daily active addresses:

Blockchain profitability

Rather than fixating on active addresses to study blockchain activity, you’re likely better off looking at network fee metrics. Fees tell you the total gas spent to use a protocol, putting aside the question of “quality” users.

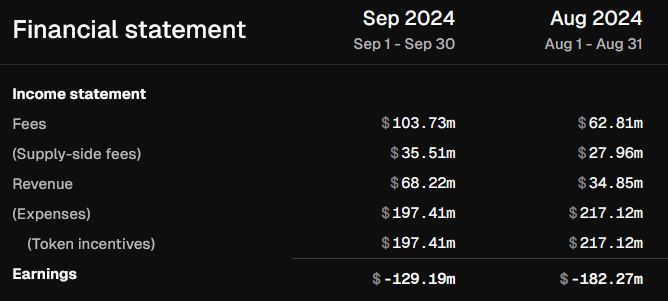

Fees are popularly used by analysts and investors to get a sense of which blockchains are generating the most “revenue.” After which, we deduct what the blockchain gives out in token issuance to validators as a cost item.

The result? Blockchain “profitability.”

That is the explicit way Token Terminal generates “financial statements” for crypto protocols. The image below, for instance, tells you that the Ethereum L1 has racked up staggering multi-million dollar losses in the last two months.

The only problem is this does not account for one crucial factor: Unlike a PoW chain like Bitcoin, users on a PoS chain can easily reap the benefits of token issuance rewards too.

After all, why would I care if a network is “unprofitable” if I’m generating a 5% yield on my staked ETH/SOL from a liquid staking platform like Lido or Jito? Treating token issuance as a cost item therefore produces a questionable conclusion that “Ethereum is unprofitable.”

Inflation is bad in the real world because when the central bank’s money printer goes “brrr,” an inflated money supply reaches different actors in the economy at different times, benefiting those who receive the new money supply first before “real” prices adjust. This is known as the Cantillon effect.

It is not, in fact, what happens in a PoS blockchain economy, since inflation (i.e. token issuance) is received by everyone at the same time. No one is made richer or poorer — everyone stays equally wealthy.

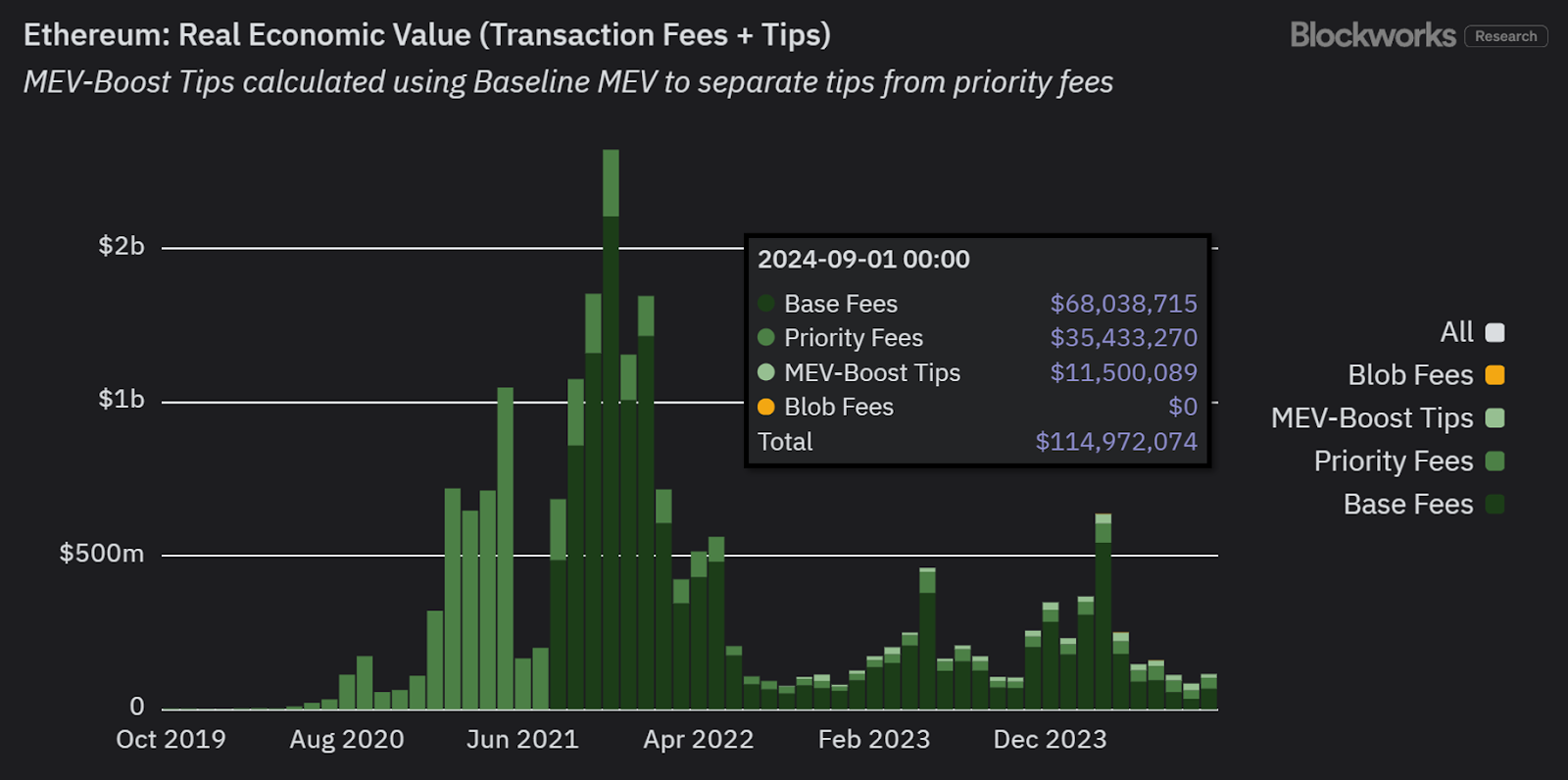

Instead, consider the alternative metric of real economic value (REV), which combines network fees and MEV tips (to validators), but leaves out issuance as a cost-item.

On that basis, we can see that Ethereum was in fact profitable over the last two months:

REV is arguably a better metric to assess the real demand of a certain network, and a more comparable apples-to-apples revenue metric to TradFi.

The long and short of it is: Traditional profit and loss ways of accounting don’t map over easily to a blockchain.

For more on this complex topic, see this recent Bell Curve podcast with Jon Charbonneau.

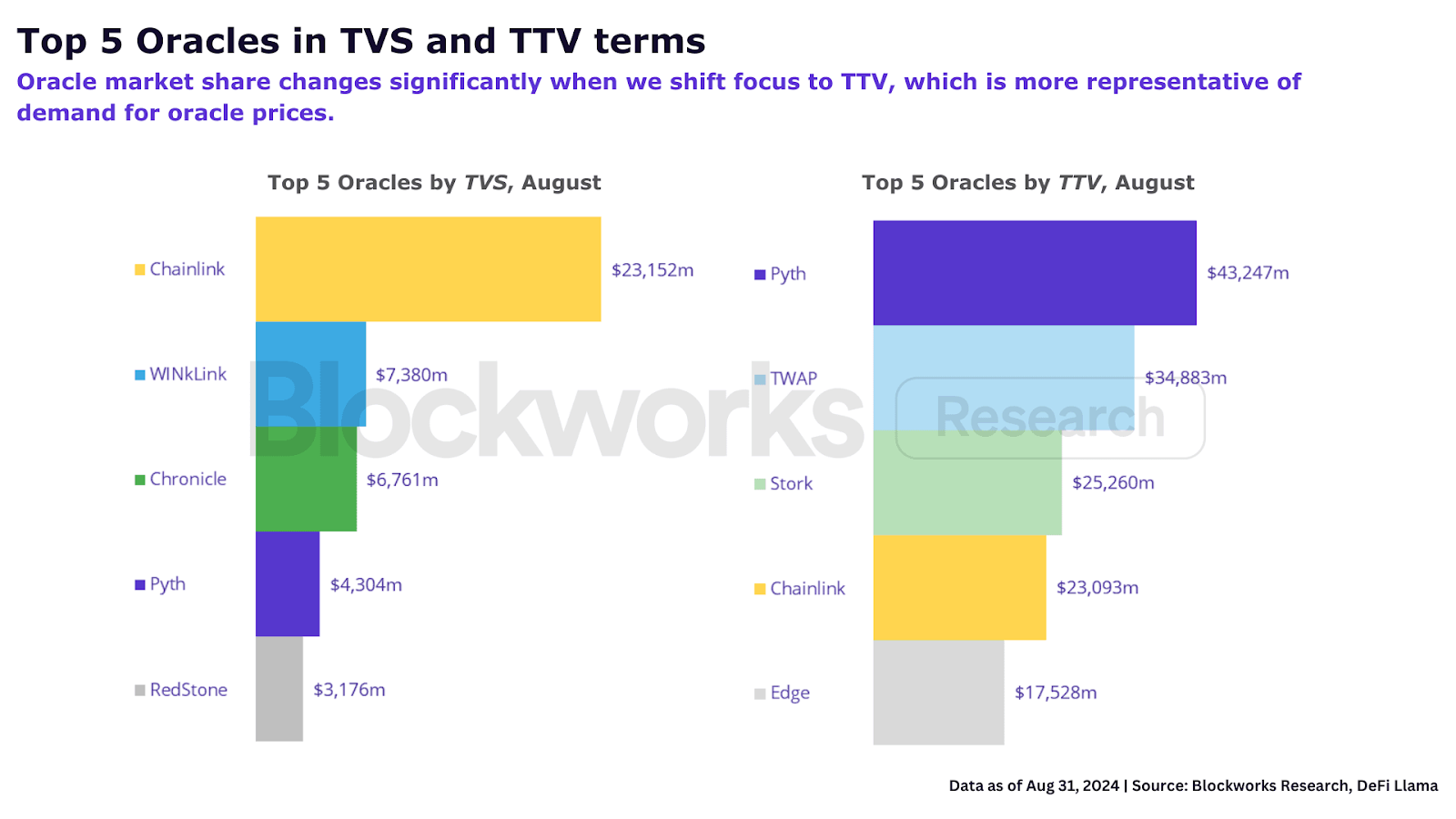

Total transaction value (TTV), not total value secured (TVS)

Oracles are a key piece of infrastructure for a blockchain to provide data access from off-chain sources. Without oracles like Chainlink, there would be no reliable way for blockchain economies to reflect prices based on the real-world economy.

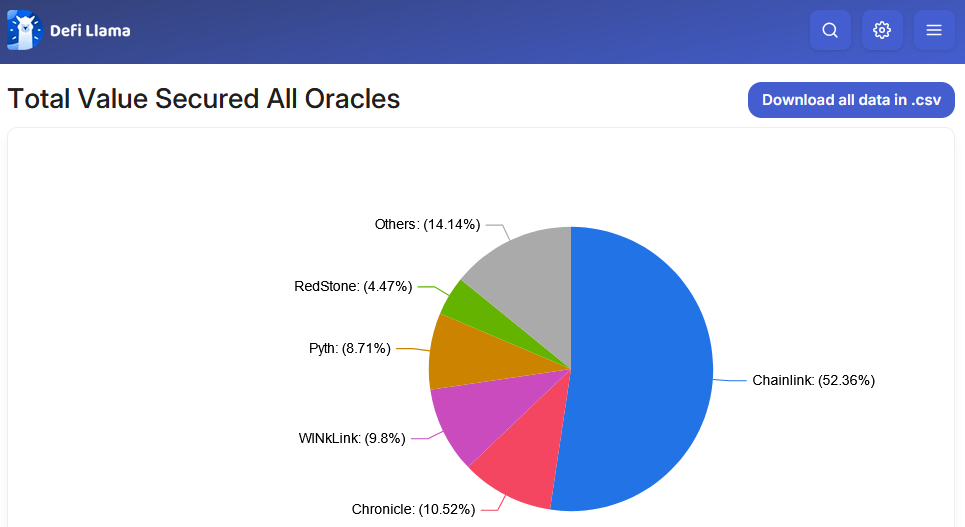

The typical way to compare market share between oracle providers is to use the “total value secured” (TVS) metric, which sums up all TVL secured by an oracle. This is explicitly how DefiLlama does it:

One problem with TVS is that it obscures the actual activity secured by an oracle.

For instance, an oracle that powers high-frequency trading products like a perpetuals exchange is constantly “pulling” price updates from an off-chain feed on a sub-second latency.

This contrasts to a “push-based” oracle for a lending protocol that updates prices onchain a few times daily because there is no need to do so as frequently.

TVS looks only at the amount of value that an oracle governs, but it neglects the performance intensity of the oracle provider.

Put another way, it would be akin to saying that a gourmet steak provided the same value to a diner as a salad because they were both $50 on the menu. Surely preparing a steak required far more work than a simple salad, a factor worth considering.

An alternative metric, such as total transaction value (TTV), would instead consider the periodic transactional volume that uses oracle updates for pricing.

TTV excludes low transaction frequency applications like lending, CDP and restaking, but as Ryan Connor explains, “2-9% of oracle price updates come from low frequency protocols, which is a very small number in the context of crypto, where volubility of fundamental measures is very high.”

When oracles are assessed based on TTV, the market share changes dramatically.

For more on this, see Blockworks Research’s report on how TTV best reflects oracle fundamentals.

Chart of the Day

Ethereum blob data nears target limit:

The Ethereum Dencun hard fork (EIP-4844) in March introduced “blobspace,” an alternative way for L2 rollups to post their batched data cheaply to the L1. Blobs are governed by a separate fee mechanism from Ethereum’s blockspace and are 10x cheaper as well as a crucial aspect of the rollup-centric roadmap. Blobs are currently limited to six blobs per L1 block (Vitalik recently called for a 33% increment).

The amount of blob data being used by Ethereum L2s is once again nearing its three-block target (the green line above), after which blobspace usage would be subject to the market forces of demand and supply. When four or more blobs are filled in the current block, the base fees for the next block increases by up to 12.5%.

Start your day with top crypto insights from David Canellis and Katherine Ross. Subscribe to the Empire newsletter.

Explore the growing intersection between crypto, macroeconomics, policy and finance with Ben Strack, Casey Wagner and Felix Jauvin. Subscribe to the Forward Guidance newsletter.

Get alpha directly in your inbox with the 0xResearch newsletter — market highlights, charts, degen trade ideas, governance updates, and more.

The Lightspeed newsletter is all things Solana, in your inbox, every day. Subscribe to daily Solana news from Jack Kubinec and Jeff Albus.